R软件与多股票波动性及相关性的可视化

前言

在量化投资建模过程之前,有时候,我们需要对多只股票的价格走势、收益率序列、波动率等进行分析。下面给出使用 R 语言比较多只股票价格走势的完整解决方案。方案涵盖数据获取、清洗、可视化及基础分析全流程:

数据获取

安装与加载工具包

# 安装必要包(首次运行需取消注释)

# install.packages(c("quantmod",

# "tidyverse",

# "ggplot2",

# "zoo",

# "corrplot"))

library(quantmod) # 获取金融数据

library(tidyverse) # 数据处理

library(ggplot2) # 可视化

library(zoo) # 时间序列处理

定义股票代码与时间范围

# 股票代码列表(支持多市场,如A股需加 .SS/.SZ)

# 苹果、谷歌、微软、英伟达

stocks <- c("AAPL", "GOOGL", "MSFT", "NVDA")

# 时间范围

start_date <- "2023-01-01"

end_date <- Sys.Date() # 获取当前日期

批量获取股票数据

# 获取数据

getSymbols(stocks,

src = "yahoo",

from = start_date,

to = end_date)

## [1] "AAPL" "GOOGL" "MSFT" "NVDA"

# 处理数据

stock_data <- lapply(stocks, function(x) {

data <- as_tibble(get(x)) %>%

mutate(Date = index(get(x))) %>%

rename_with(~ gsub(paste0("^", x, "\\."), "", .x)) %>%

select(Date, Close) %>%

mutate(symbol = x) %>% # 添加股票代码列

rename(price = Close) # 重命名收盘价列

}) %>%

bind_rows()

# 查看结果

head(stock_data)

## # A tibble: 6 × 3

## Date price symbol

## <date> <dbl> <chr>

## 1 2023-01-03 125. AAPL

## 2 2023-01-04 126. AAPL

## 3 2023-01-05 125. AAPL

## 4 2023-01-06 130. AAPL

## 5 2023-01-09 130. AAPL

## 6 2023-01-10 131. AAPL

数据清洗

处理缺失值

library(dplyr)

# 检查缺失值

missing_values <- stock_data %>%

group_by(symbol) %>%

summarise(missing = sum(is.na(price)))

# 填充缺失值(使用前向填充)

stock_data <- stock_data %>%

group_by(symbol) %>%

mutate(price = na.locf(price))

对齐时间序列

library(dplyr)

# 生成完整日期序列

full_dates <- tibble(Date = seq(as.Date(start_date),

as.Date(end_date),

by = "day"))

# 左连接填充所有日期

stock_data <- full_dates %>%

left_join(stock_data, by = "Date") %>%

group_by(symbol) %>%

fill(price, .direction = "downup") %>%

na.omit()

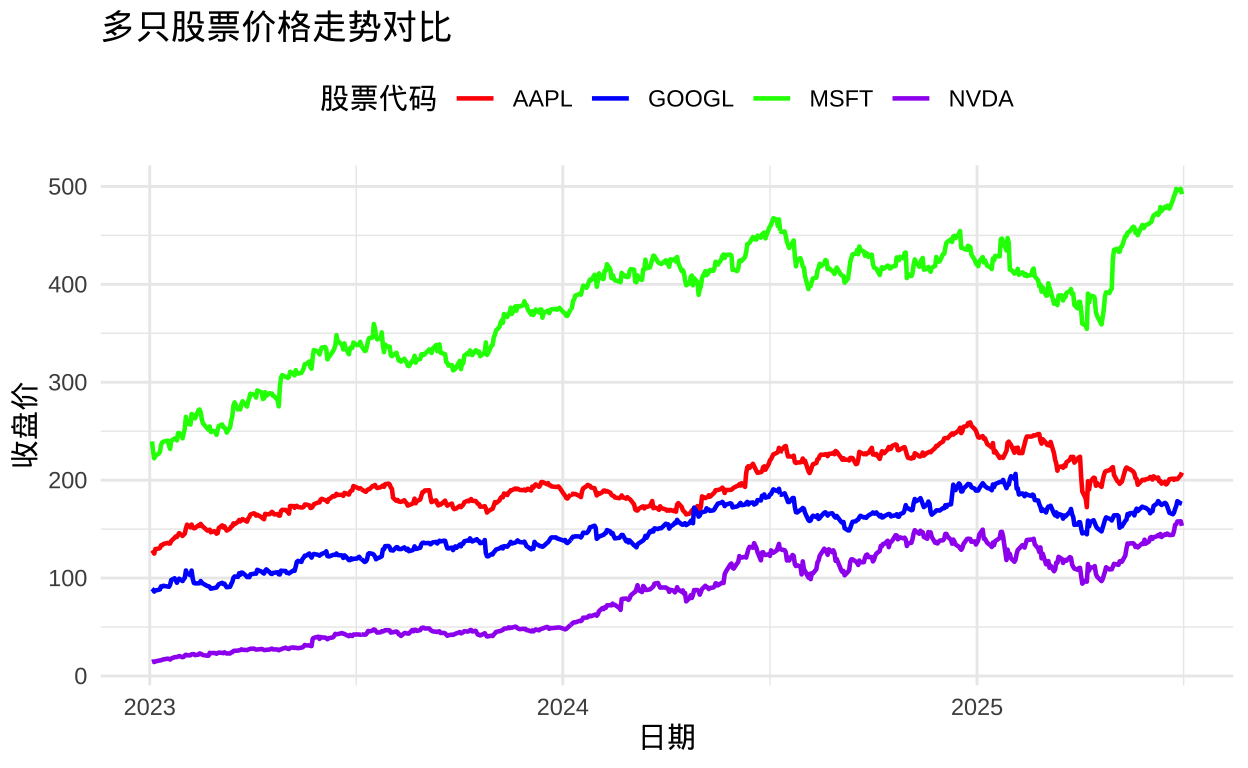

价格走势可视化

基础折线图

library(dplyr)

ggplot(stock_data, aes(x = Date, y = price, color = symbol)) +

geom_line(linewidth = 0.8) +

labs(title = "多只股票价格走势对比",

x = "日期",

y = "收盘价",

color = "股票代码") +

theme_minimal() +

theme(legend.position = "top") +

scale_color_manual(values = c("AAPL" = "red",

"GOOGL" = "blue",

"MSFT" = "green",

"NVDA" = "purple")

)

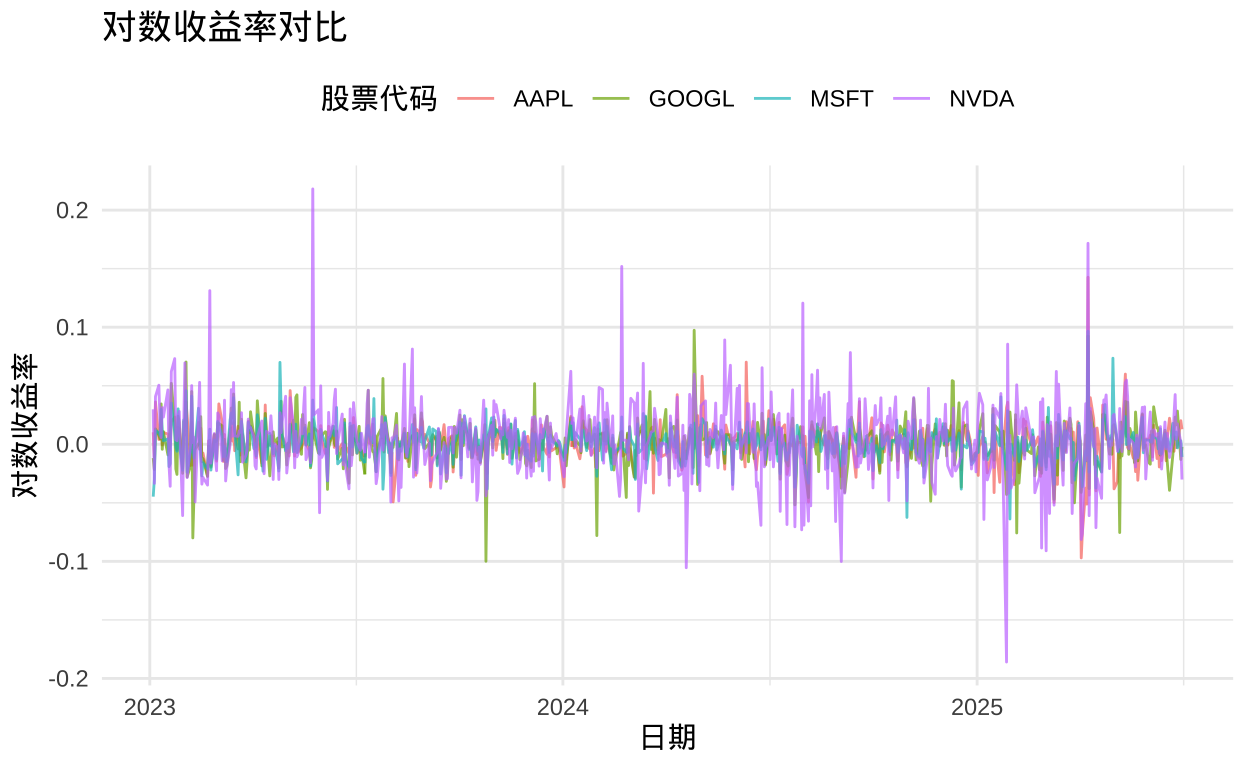

对数收益率对比

library(dplyr)

# 计算对数收益率

return_data <- stock_data %>%

group_by(symbol) %>%

mutate(log_return = log(price) - log(lag(price))) %>%

na.omit()

# 绘制收益率曲线

ggplot(return_data,

aes(x = Date, y = log_return, color = symbol)) +

geom_line(alpha = 0.7) +

labs(title = "对数收益率对比",

x = "日期",

y = "对数收益率",

color = "股票代码") +

theme_minimal() +

theme(legend.position = "top") # 图例放底部

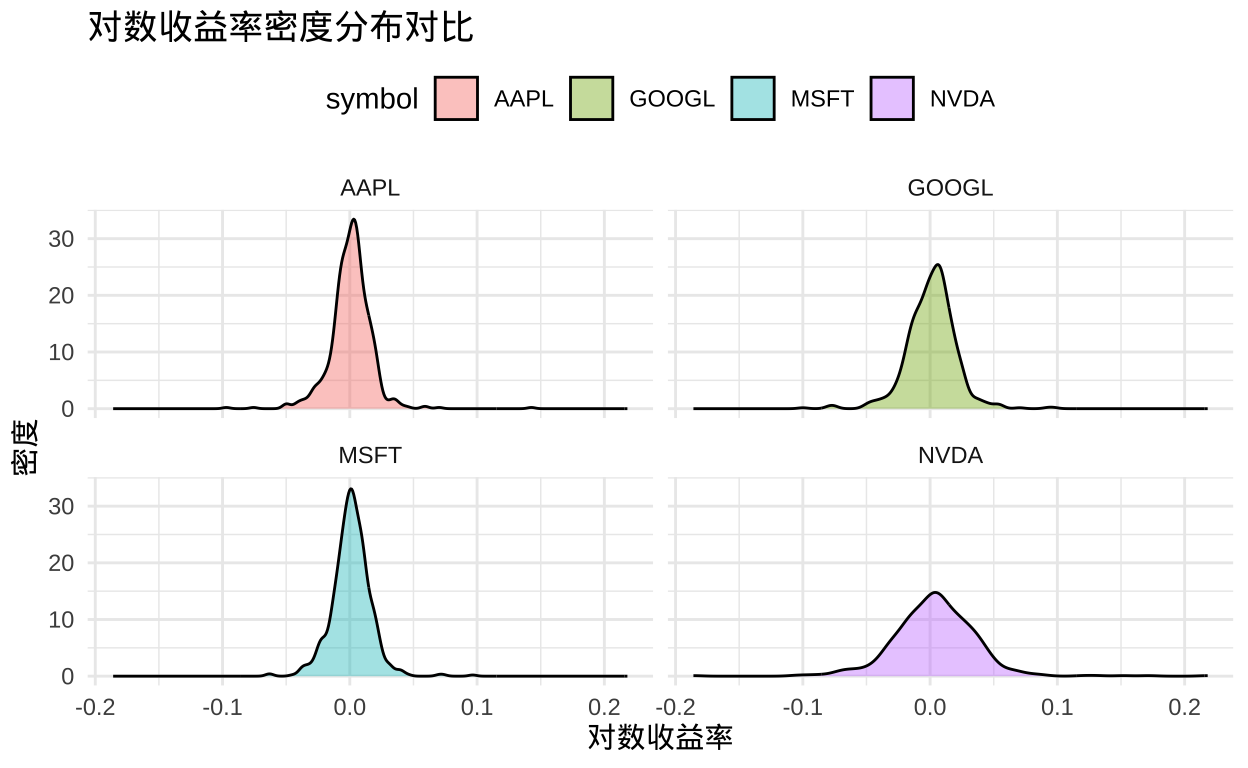

绘制对数收益率密度图:

library(dplyr)

ggplot(return_data, aes(x = log_return, fill = symbol)) +

geom_density(alpha = 0.4) + # 半透明填充

facet_wrap(~ symbol, ncol = 2) + # 按股票分面显示

labs(title = "对数收益率密度分布对比",

x = "对数收益率",

y = "密度") +

theme_minimal() +

theme(legend.position = "top") # 图例放底部

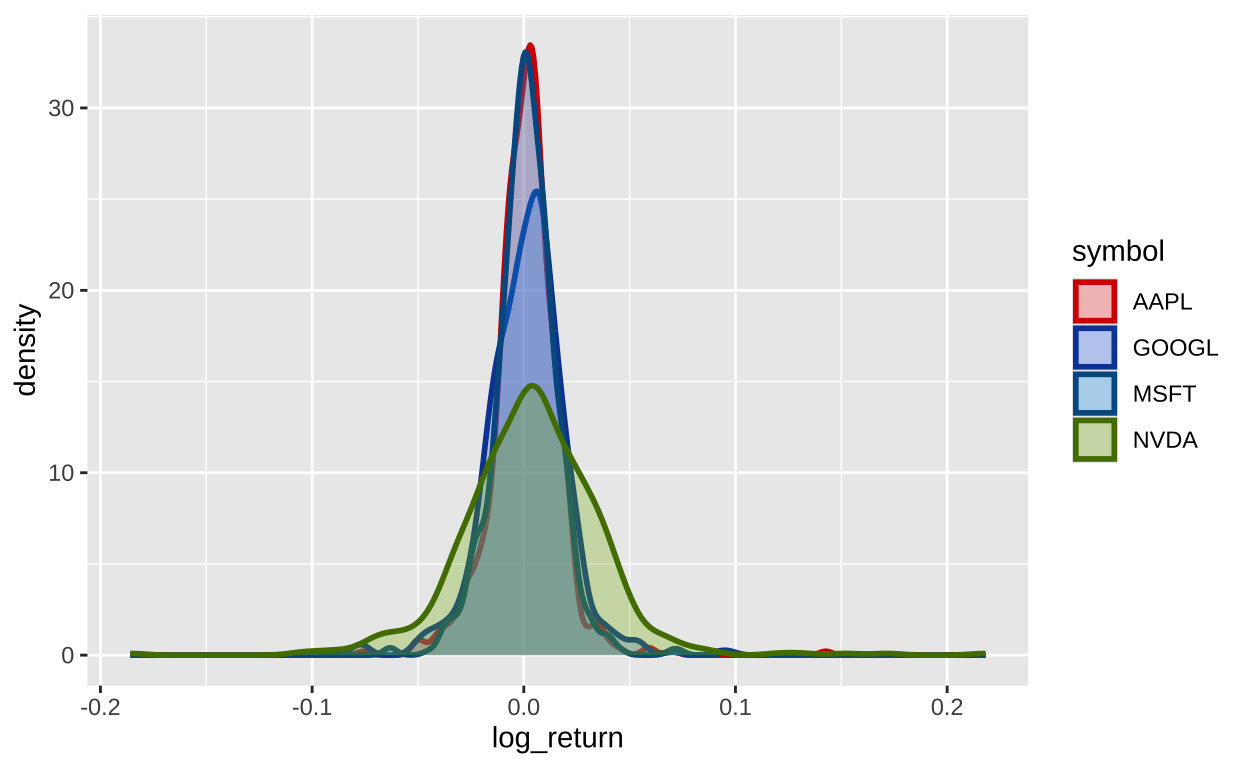

将密度图叠加以便于比较:

library(dplyr)

# 对数收益率密度图(叠加显示)

ggplot(return_data, aes(x = log_return, fill = symbol, color = symbol)) +

geom_density(alpha = 0.3, linewidth = 1) +

scale_fill_manual(values = c("AAPL" = "#FF5252",

"GOOGL" = "#4285F4",

"MSFT" = "#00A4EF",

"NVDA" = "#7FBA00")) +

scale_color_manual(values = c("AAPL" = "#D50000",

"GOOGL" = "#0D47A1",

"MSFT" = "#005A8E",

"NVDA" = "#527D00"))

labs(title = "对数收益率密度分布对比",

x = "对数收益率",

y = "密度",

fill = "股票代码",

color = "股票代码") +

theme_minimal() +

theme(

legend.position = "top",

legend.box = "horizontal",

plot.title = element_text(hjust = 0.5, size = 14, face = "bold"),

axis.title = element_text(size = 12),

axis.text = element_text(size = 10)

)

## NULL

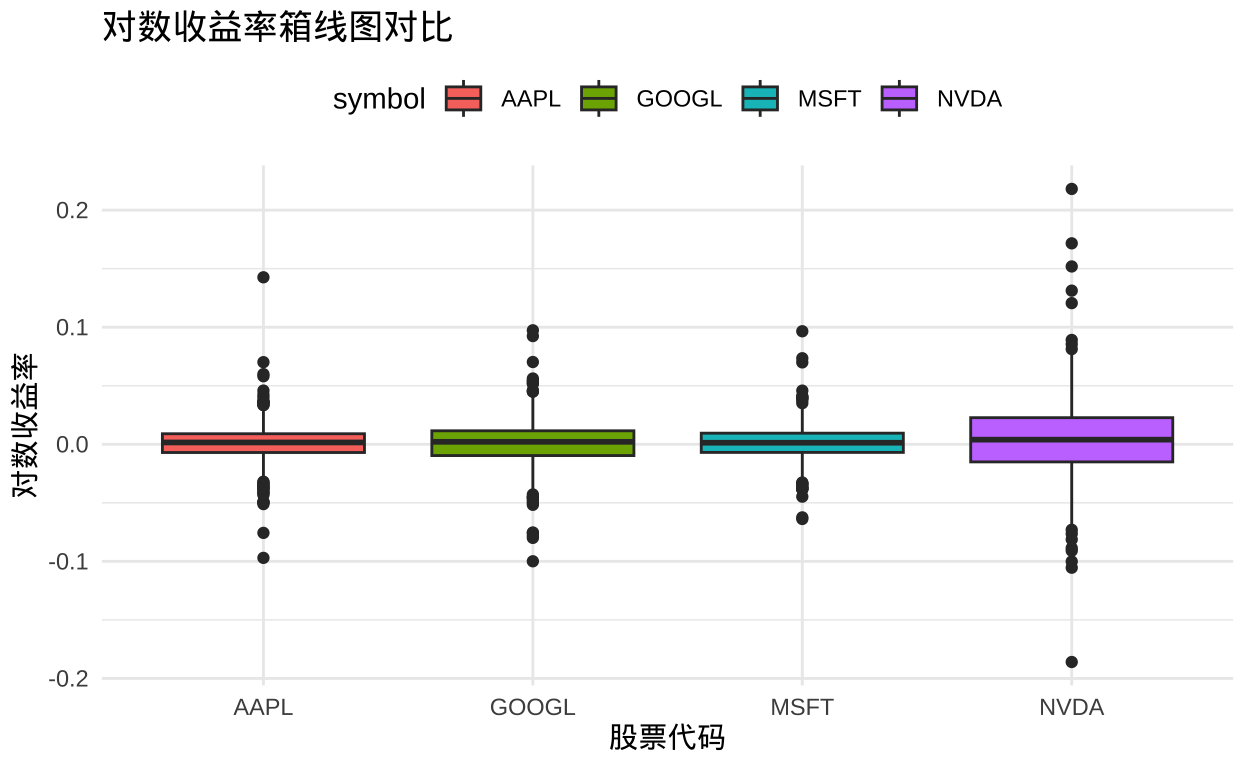

还可以绘制箱线图:

library(dplyr)

# 箱线图对比

ggplot(return_data, aes(x = symbol, y = log_return, fill = symbol)) +

geom_boxplot() +

labs(title = "对数收益率箱线图对比",

x = "股票代码",

y = "对数收益率") +

theme_minimal() +

theme(legend.position = "top")

股票数据特征的统计分析

计算波动率

library(dplyr)

volatility <- return_data %>%

group_by(symbol) %>%

summarise(volatility = sd(log_return, na.rm = TRUE)) %>%

arrange(desc(volatility))

print(volatility)

## # A tibble: 4 × 2

## symbol volatility

## <chr> <dbl>

## 1 NVDA 0.0314

## 2 GOOGL 0.0191

## 3 AAPL 0.0161

## 4 MSFT 0.0146

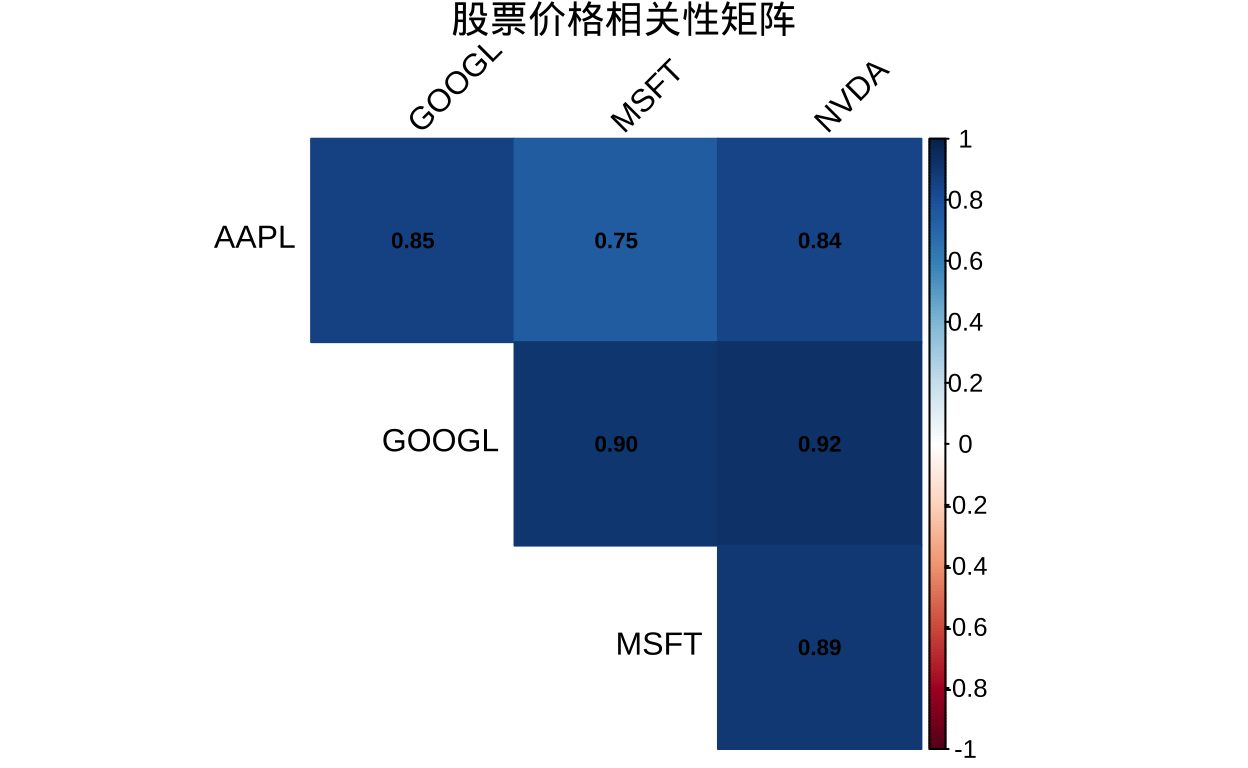

相关性分析

library(dplyr)

# 转换为宽格式

price_wide <- return_data %>%

select(Date, symbol, price) %>%

pivot_wider(names_from = symbol, values_from = price) %>%

column_to_rownames(var = "Date")

# 计算相关系数矩阵

cor_matrix <- cor(price_wide)

# 可视化相关系数

library(corrplot)

# 绘制相关性矩阵(暖色调)

corrplot(cor_matrix,

method = "color", # 颜色填充

type = "upper", # 只显示上三角

tl.col = "black", # 标签颜色

tl.srt = 45, # 标签倾斜角度

title = "股票价格相关性矩阵",

mar = c(0,0,1,0), # 边距调整

addCoef.col = "black", # 添加相关系数数值

number.cex = 0.7, # 系数文字大小

diag = FALSE) # 不显示对角线

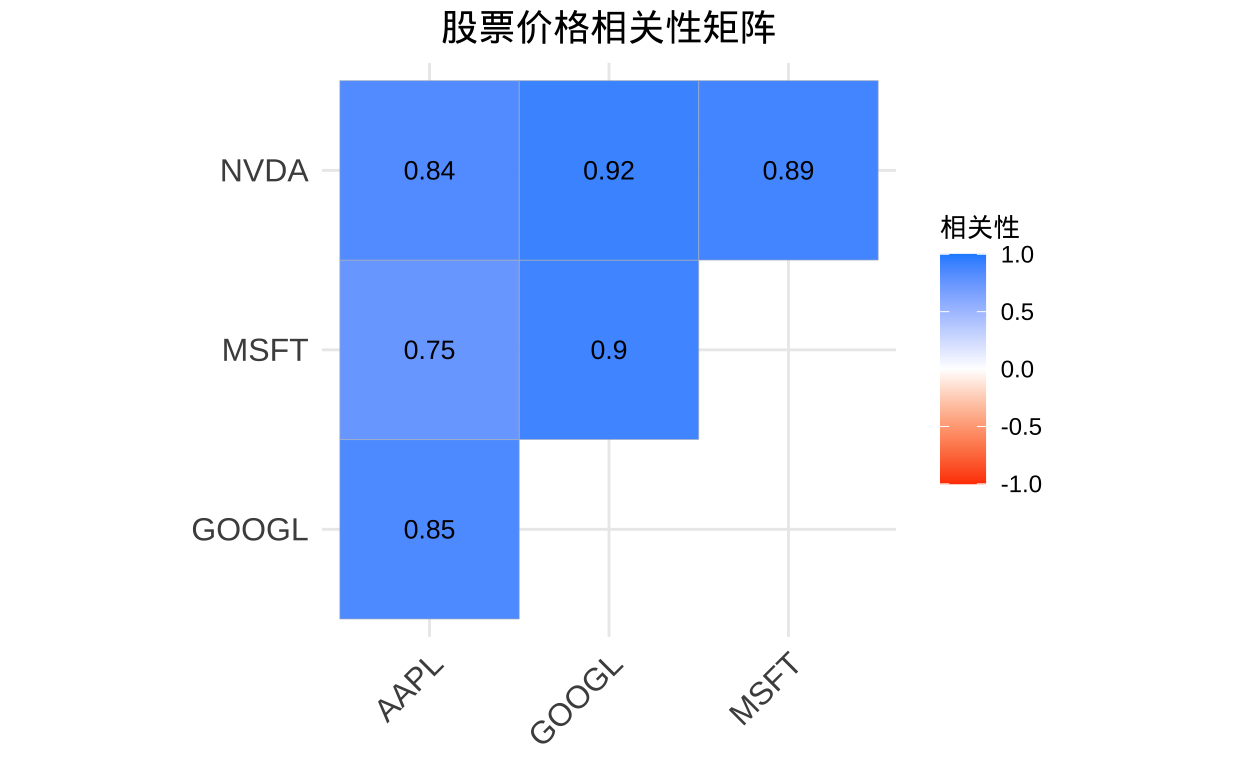

# 计算相关系数矩阵

cor_matrix <- cor(price_wide)

# 使用ggcorrplot绘制ggplot2风格的相关性矩阵(暖色调)

library(ggcorrplot)

ggcorrplot(

cor_matrix,

method = "square", # 颜色填充

type = "upper", # 只显示上三角

colors = c("#FF4500", "#FFFFFF", "#1E90FF"), # 自定义颜色(红-白-蓝)

lab = TRUE, # 显示相关系数

lab_size = 3.5, # 系数文字大小

title = "股票价格相关性矩阵",

ggtheme = theme_minimal(), # ggplot2主题

show.legend = TRUE, # 显示图例

legend.title = "相关性",

tl.col = "black", # 标签颜色

tl.srt = 45, # 标签倾斜角度

digits = 2 # 保留两位小数

) +

theme(

plot.title = element_text(hjust = 0.5, size = 14, face = "bold"),

axis.text = element_text(size = 10),

legend.text = element_text(size = 9),

legend.title = element_text(size = 10, face = "bold")

)

导出数据

# 导出为 CSV

# write_csv(stock_data, "stock_prices.csv")

# 导出为 Excel(需安装 writexl 包)

# install.packages("writexl")

# write_xlsx(stock_data, "stock_prices.xlsx")

小结

本文的数据来源为雅虎财经(Yahoo Finance),若需更专业数据,可考虑 WRDS 数据库(需机构订阅)。

在 R 软件包的选择上,我们使用了 quantmod 包以快速获取数据,但该软件包返回的是 xts 格式,后续计算过程中需转换为 tibble 。

数据处理过程借助于 tidyquant 包,该软件包可以返回整洁格式的数据,与 tidyverse 兼容性更好。

缺失值处理方面,前向填充(na.locf)适用于短期缺失,多重插补(mice包)可处理复杂缺失模式。可视化优化方面,可以使用scale_color_manual自定义颜色。此外,可以添加geom_smooth拟合趋势线(如method = “loess”)。

通过以上步骤,我们可以高效地获取、清洗并可视化多只股票的价格走势,结合波动率和相关性分析,为投资决策提供数据支持。